Investor

Presentation Investor Presentation

Exhibit 99.1 |

| Investor

Presentation Investor Presentation

Exhibit 99.1 |

Safe

Harbor 2

This

presentation

may

contain

certain

forward-looking

statements

and

management

may

make

additional

forward-looking

statements

in

response

to

your

questions.

These

statements

do

not

guarantee

future

performance

and

speak

only

as

of

the

date

hereof,

and

qualify

for

the

safe

harbor

provided

by

Section

21E

of

the

Securities

Exchange

Act

of

1934,

as

amended,

and

Section

27A

of

the

Securities

Act

of

1933.

We

refer

all

of

you

to

the

risk

factors

contained

in

US

Auto

Parts

Annual

Report

on

Form

10-K

and

quarterly

reports

on

Form

10-Q

filed

with

the

Securities

and

Exchange

Commission,

for

more

detailed

discussion

on

the

factors

that

can

cause

actual

results

to

differ

materially

from

those

projected

in

any

forward-looking

statements. |

Case

for Investment 3

Large and Growing Online Market

Significant Customer Reach

Significant Private Label Offering

Reduced Cost Structure

No Debt

Experienced Leadership Team |

4

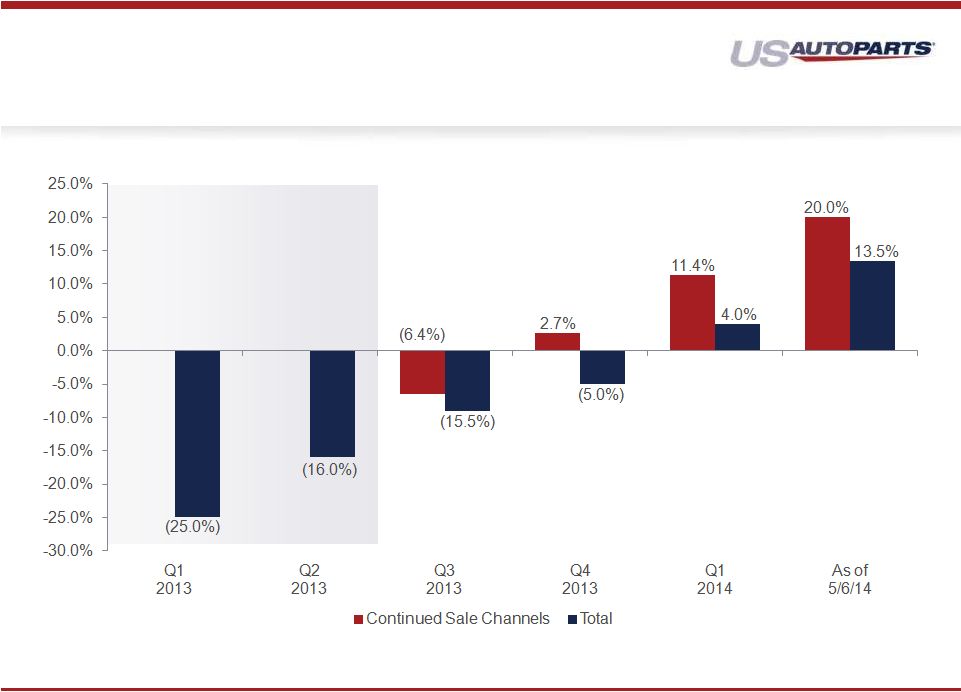

Go forward sales channels up 11% with total comps up 4%

As of 5/6 go forward trend for Q2 trending up 20% and overall

comps up 13%

Adjusted EBITDA was $3.3M up from $1.5M in Q1-13

Adjusted EBITDA less CAPEX was $1.8M up from ($1.1M) in Q1-13

As of 5/6 -

$3M of cash on the balance sheet with no debt

Highlights from Q1-14

Earnings Call |

5

Completed the retirement of a number of websites by the end of 2Q ‘13

Recent Revenue Trends |

Sales & Adjusted EBITDA

6

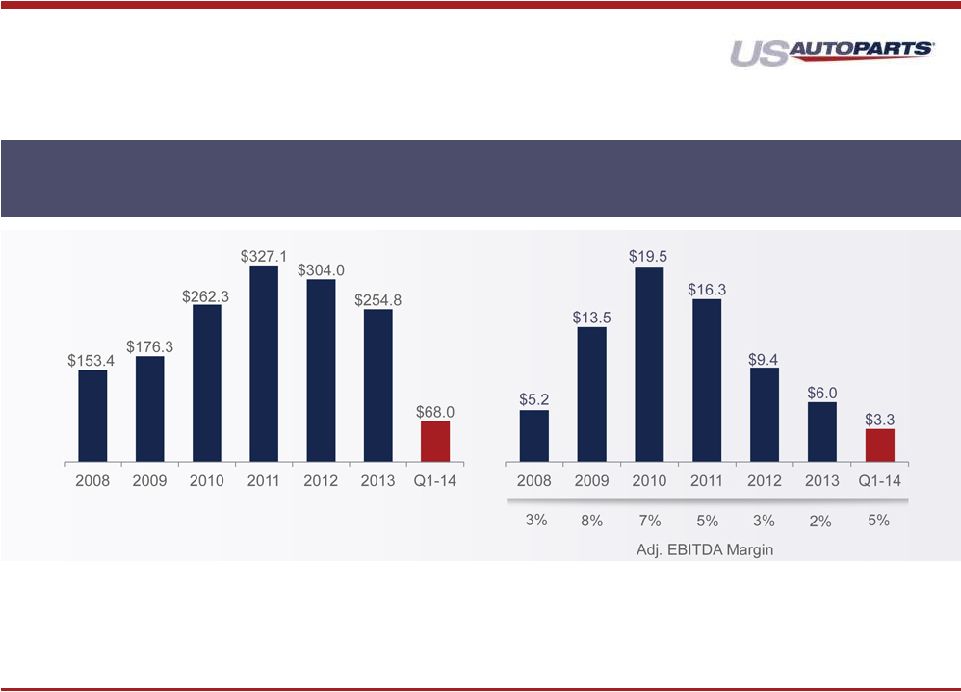

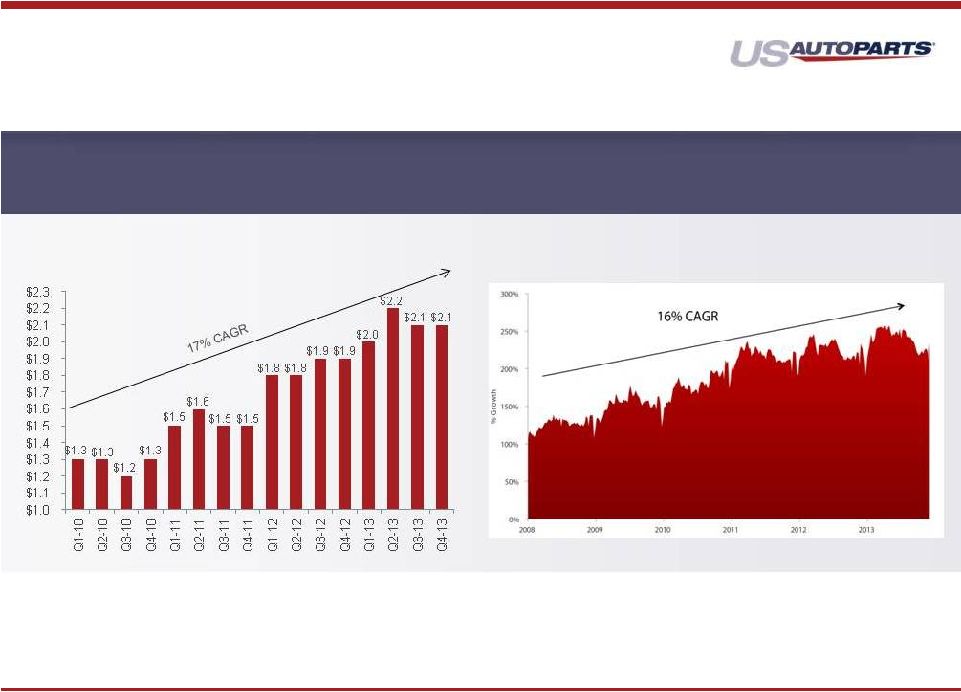

1.

JC

Whitney

was

acquired

in

Aug

2010

adding

revenue

of

$39.1M

in

2010

and

$83.4M

in

2011.

Amounts

not

separately

disclosed

after

2011.

2.

Non-GAAP

financial

measure

EBITDA

consists

of

net

income

before

(a)

interest

expense,

net;

(b)

income

tax

provisions;

(c)

amortization

of

intangible

assets;

(d)

depreciation

and

amortization.

Adjusted

EBITDA

excludes

Stock

based

compensation

of

$2.9M,

$3.3M,

$2.7M,

$2.6M,

$1.7M

,

$1.3M

and

$0.4M

in

2008,

2009,

2010,

2011,

2012,

2013

and

Q1-14,

respectively

and

restructuring

costs

and

other

one

time

charges

of

$23.4M,

$0.4M,

$5.8M,

$12.9M,

$27.5M

and

$6.8M

in

2008,

2009,

2010,

2011,

2012

and

2013,

respectively.

There

were

no

restructuring

or

one

time

charges

in

Q1-14.

Consolidated Sales

1

($ In Millions)

Consolidated Adjusted EBITDA

2

($ In Millions) |

7

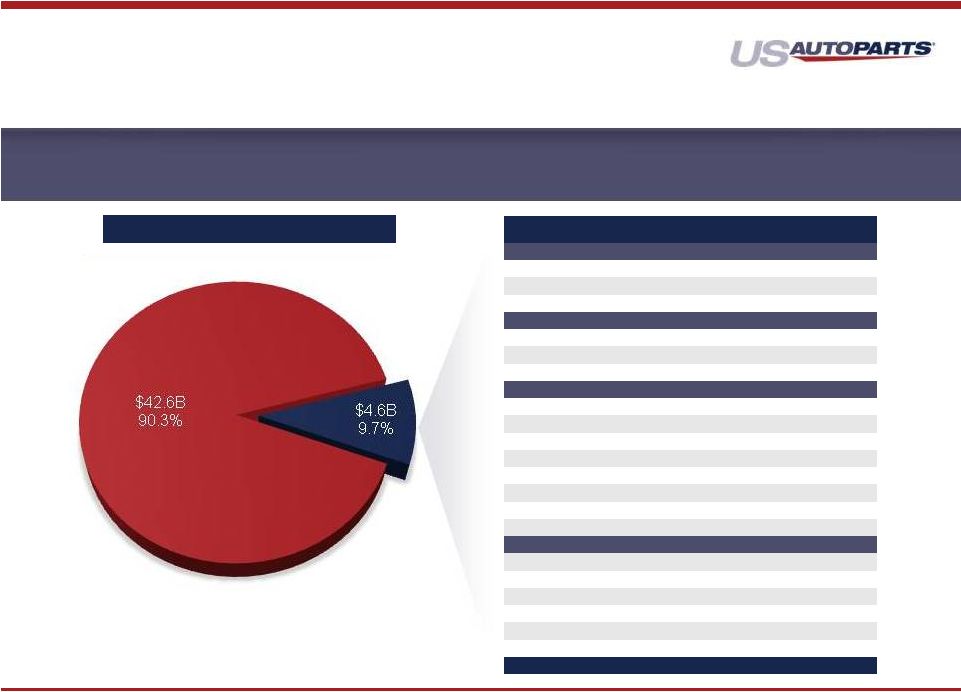

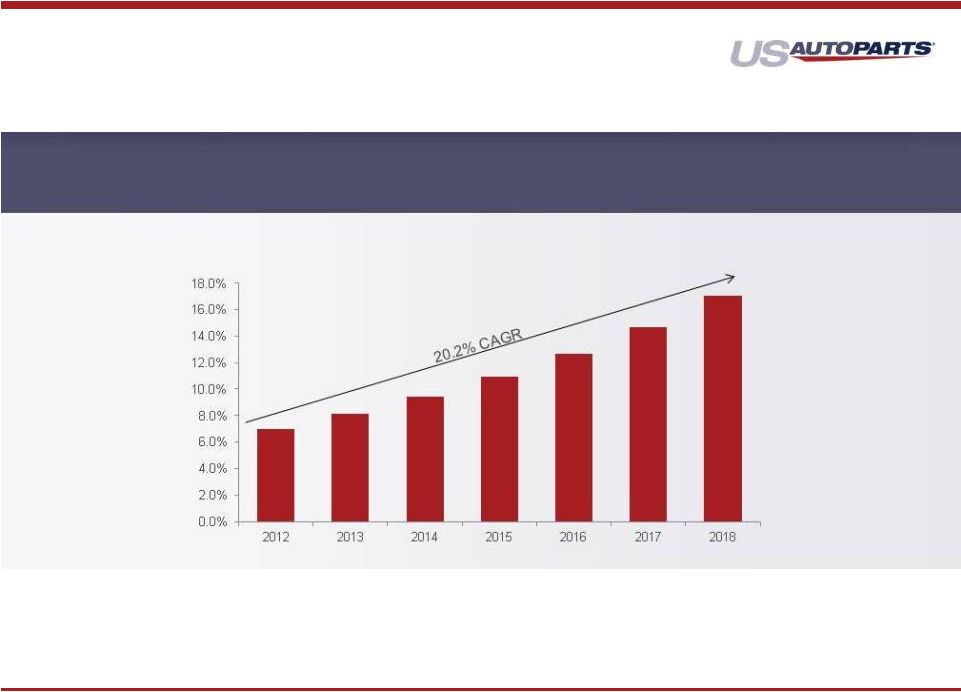

At 9.7% online market penetration, auto parts still lags industry average in the

teens. US Auto Parts is the largest pure-play online retailer of auto

parts 1

AASA

estimates

2

Estimates

by

US

Auto

Parts

where

amounts

are

not

publicly

reported

&

we

estimate

the

total

online

DIY

market

to

be

larger

than

the

$3.8B

that

is

reported

in

the

2014

AAIA

Fact

Book

3

Excludes

AutoAnything

which

is

wholly

owned

by

AutoZone

Do It Yourself (DIY) Market Size

Company

2013 Est. Rev

2

% of total

Marketplaces

(in million)

eBay Motors

$2,200

47.6%

Amazon

$600

13.0%

Sub Total

$2,800

60.6%

Wholesale Online

Tire Rack (online)

$440

9.5%

Other Tire Companies

$190

4.1%

Sub Total

$630

13.6%

Pure Play

USAP

$250

5.4%

Rock Auto

$180

3.9%

Summit

$170

3.7%

Auto Anything

(AutoZone)

$120

2.6%

JEGS

$70

1.5%

CarID

$60

1.3%

All Other Pure Play

$90

1.9%

Sub Total

$940

20.3%

Brick & Mortar Retailers

AutoZone (w/o AA)

3

$110

2.4%

Advance

$80

1.7%

Pep

$30

0.6%

O'Reilly

$20

0.4%

NAPA

$10

0.2%

Sub Total

$250

5.4%

Total

4,620

100.0%

Total

DIY

Market

Size

for

2013

of

47.2B

1 |

Source: Google

8

eBay Parts Sales Continue to Increase

Source: eBay filings, press releases

Google Queries for Parts Growing

Online Market is Vibrant and Growing

Aftermarket e-Commerce Overview

Online sales of automotive parts and accessories have grown in the high

teens and are expected to grow at 20% going forward |

Booz & Co. estimates by 2018 that Online DIY could reach 17%

of the total DIY market

9

Online Market is Vibrant and Growing

Aftermarket e-Commerce Overview

DIY Online Penetration |

10

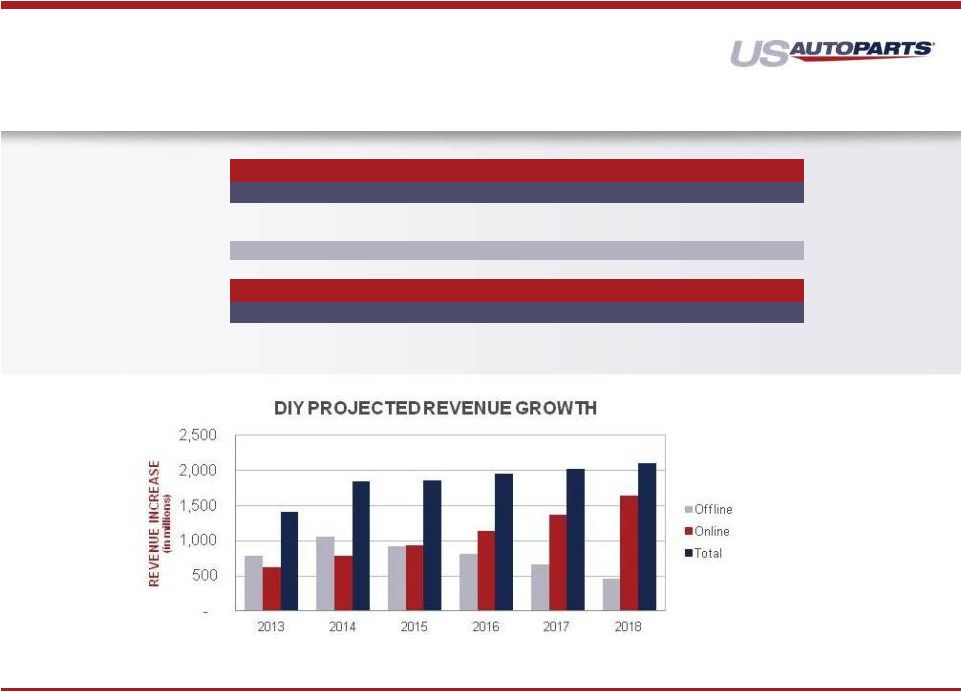

Do It Yourself (DIY) Projections

1

DIY PROJECTED REVENUES

(in millions)

2012

2013

2014

2015

2016

2017

2018

Offline

$42,544

$43,331

$44,388

$45,306

$46,120

$46,778

$47,236

Online

3,202

3,827

4,611

5,549

6,680

8,041

9,680

$45,746

$47,158

$48,999

$50,855

$52,800

$54,819

$56,916

DIY PROJECTED MARKET SHARE

2012

2013

2014

2015

2016

2017

2018

Offline

93.0%

91.9%

90.6%

89.1%

87.3%

85.3%

83.0%

Online

7.0%

8.1%

9.4%

10.9%

12.7%

14.7%

17.0%

1

Projections

obtained

from

AAIA

2014

Digital

Automotive

Aftermarket

Fact

Book

and

March

2014

AASA

Digital

Disruption:

e-tailing

in

the

Automotive

Aftermarket

Report |

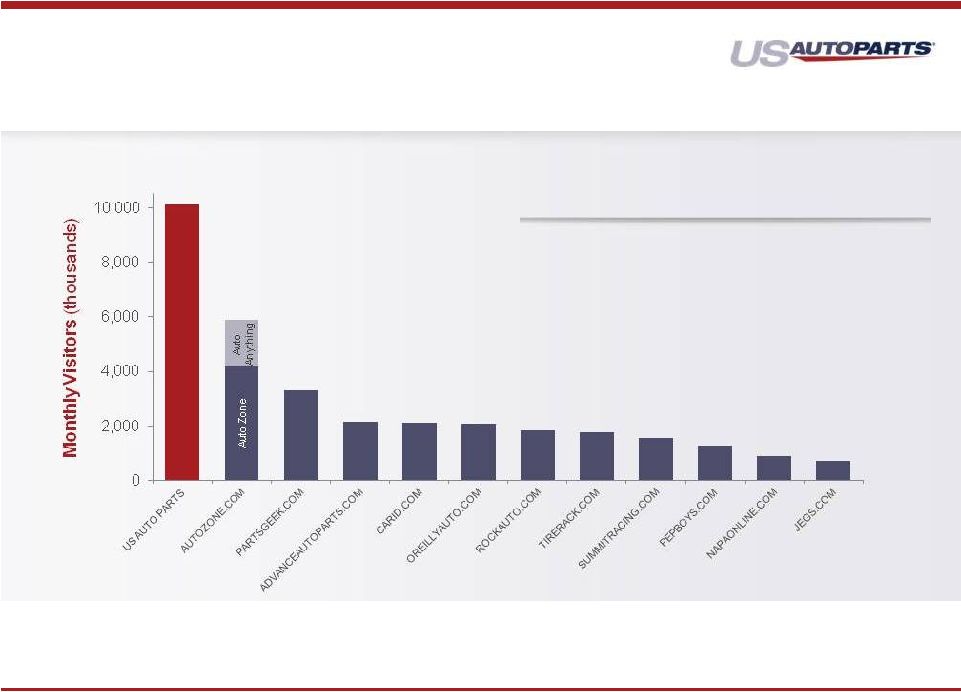

(some overlap of monthly visitors across websites)

11

USAP

traffic

includes

traffic

from

continued

sales

channels

Competitive

sites’

traffic

based

on

Compete

March

2014

reports

Customer Reach is a Competitive Moat

•

Over 500 man years of hand written unique content

•

Long domain history to help indexing in search

•

Multiple website management

US Auto Parts Dominant Reach-

Largest Pure Play Internet Retailer |

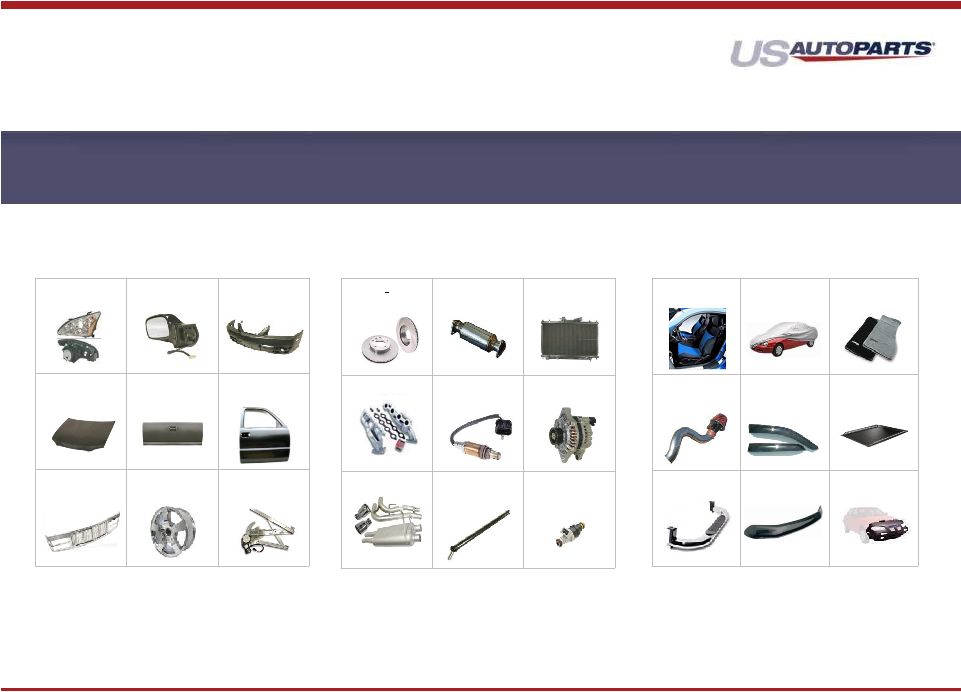

12

Brake

Discs

Catalytic

Converters

Radiators

Headers

Oxygen

Sensors

Alternators

Exhaust

Driveshaft

Fuel Injection /

Delivery

Lamps

Mirrors

Bumpers

Hoods

Tailgates

Doors

Grills

Wheels

Window

Regulators

Seat Covers

Car Covers

Floor Mats /

Carpeting

Cold Air

Intakes

Vent Visors

Tonneau

Covers

Nerf Bars

Bug Shields

Car Bras

Body Parts

Engine Parts

Performance & Accessories

*Represents

USAP

online

mix

36%

48%

16%

Revenue*

US

Auto

Parts

has

one

of

the

largest

product

offerings

with

over

1.5

million

products

across

body

parts,

engine

parts,

and

performance

&

accessories

Broad Auto Parts Product Offering |

USAP’s ability to competitively price products while maintaining healthy

margins is a function of the Company’s ability to leverage its robust

private label supply chain. –

Currently over 40,000 Private Label Products.

–

Adding 4,000 –

5,000 Private Label SKUs this year

–

The Company sources product directly from over 200 factories in Asia

13

Margin %

In-Stock

Private Label

(Asia Sourced)

Branded

(U.S. Sourced)

30% -

60%

15% -

30%

5% -

20%

Drop Shipped

Current Mix

55%

45%

Current Mix

68%

32%

The breath of our Private Label products provides a significant competitive

moat USAP’s Supply Chain Creates

Pricing Advantage |

Revenue

100%

Gross Margins

27% -

29%

Variable OPEX Costs

15%

Fixed Cost

0%

Incremental Flow

12% -

14%

14

Incremental Flow Thru

Recent new trends for our go forward sales channel are growing at 20% as of the 5/6

earnings call Growth and Profitability |

15

*Excludes non-cash D&A, stock based comp and restructuring

Over $19M of costs have been reduced over a two year period

USAP has significantly reduced

operating cost

OPEX

(in

thousands)

Q1-14

% of rev

Q1-13

% of rev

$ Change

% of rev change

Fulfillment*

3,935

5.8%

3,994

6.1%

(59)

(30 bps)

Marketing*

8,691

12.8%

8,967

13.7%

(276)

(90 bps)

Technology*

1,129

1.7%

1,395

2.1%

(266)

(40 bps)

General & Administrative*

3,620

5.3%

3,873

5.9%

(252)

(60 bps)

Subtotal

17,376

25.5%

18,229

27.9%

(853)

(240 bps)

D&A and Stock Based Comp

2,829

4.2%

4,153

6.3%

(1,324)

(210 bps)

Restructuring

-

0.0%

498

0.8%

(498)

(80 bps)

Total OPEX

20,205

29.7%

22,880

35.0%

(2,675)

(530 bps)

Fixed Cost

7,206

10.6%

8,253

12.6%

(1,047)

(200 bps)

Variable

10,170

14.9%

9,976

15.3%

193

40 bps

D&A & Stock Based Comp

2,829

4.2%

4,153

6.3%

(1,324)

(210 bps)

Restructuring

-

0.0%

498

0.8%

(498)

(80 bps)

Total

20,205

29.7%

22,880

35.0%

(2,675)

(530 bps)

CAPEX

1,558

2.3%

2,623

4.0%

(1,065)

(170 bps)

Total OPEX & CAPEX

21,763

32.0%

25,503

39.0%

(3,740)

(700 bps)

Annualized

87,053

102,012

(14,959) |

Base

8%

18%

27%

37%

Revenue

$255

$275

$300

$325

$350

Gross Margin %

27.0%

–

29.0%

27.0%

–

29.0%

27.0%

–

29.0%

27.0%

–

29.0%

27.0%

–

29.0%

Variable:

Fulfillment

3.4%

3.4%

3.4%

3.4%

3.4%

Marketing

9.2%

9.2%

9.2%

9.2%

9.2%

Technology

0.6%

0.6%

0.6%

0.6%

0.6%

G&A

1.7%

1.7%

1.7%

1.7%

1.7%

Total Variable

14.9%

14.9%

14.9%

14.9%

14.9%

Fixed:

Fulfillment

2.5%

2.3%

2.1%

2.0%

1.8%

Marketing

3.8%

3.5%

3.2%

3.0%

2.8%

Technology

1.1%

1.1%

1.0%

0.9%

0.8%

G&A

3.8%

3.5%

3.2%

3.0%

2.8%

Total Fixed

11.2%

10.4%

9.5%

8.8%

8.2%

Adjusted EBITDA %

0.9%

–

2.9%

1.7%

–

3.7%

2.5%

–

4.5%

3.3%

–

5.3%

3.9%

–

5.9%

Adjusted EBITDA $

$2

–

$7

$5

–

$10

$8

–

$14

$11

–

$17

$14

–

$21

16

Our business model has significant cost leverage as revenues grow

1.

2013 Revenue was $255M

2.

Excludes stock based compensation, depreciation and amortization

3.

For every incremental year required to achieve growth levels, fixed expenses

increase $1.0M or 3% Financial Sensitivity |

17

AutoMD –

Addressing the

DIFM Market |

18

Large and Growing Online Market

Significant Customer Reach

Significant Private Label Offering

Reduced Cost Structure over

No Debt

Experienced Leadership Team

Case for Investment |

19

Shane Evangelist -

Chief Executive Officer

Chief Executive Officer since October 2007 with over 10 years of

leading internet businesses

Senior Vice President and General Manager of Blockbuster Online

Vice President of Strategic Planning for Blockbuster Inc.

B.A. degree in Business Administration from the University of New

Mexico and a M.B.A. from Southern Methodist University

David Robson -

Chief Financial Officer

Chief Financial Officer since January 2012

Over 20 years of finance, accounting, and operational experience

and

has held senior positions with both public and private companies

Executive Vice President and Chief Administrative Officer at Mervyns'

LLC, SVP of Finance and Principal Accounting Officer for Guitar

Center, Inc.

B.S. degree in Accounting from University of Southern California;

certified public accountant

Aaron E. Coleman -

Chief Operating Officer

Chief Operating Officer since September 2010, and was Executive

Vice President of Operations and CIO from April 2008 until September

2010 with over 18 years of e-commerce experience

Senior Vice President –

Online Systems at Blockbuster Inc.

Multiple positions with internet and technology companies including

American Airlines, Travelweb (Priceline), Baan

B.A. degree in Business Administration from Gonzaga University

Leadership Team

Charles Fischer -

Senior Vice President of Global Procurement

Senior Vice President of Global Sourcing and Procurement since May 2008

with over 30 years of global sourcing experience

Vice President, Supply Chain Management for Keystone Automotive Industries

Director, Business Development for Modern Engineering

Multiple leadership positions with multiple companies in the automotive

aftermarket industry |

20

Over $19M of costs have been reduced over a two year period

Adjusted EBITDA

(Non-GAAP

Financial

Measure

–

in

thousands)

Thirteen Weeks Ended

March 29

March 30

2014

2013

Net income (loss)

201

$

(3,343)

$

Interest expense, net

259

185

Income tax provision

32

21

Amortization of intangible assets

84

106

Depreciation and amortization expense

2,368

3,638

EBITDA

2,944

607

Share-based compensation expense

376

409

Restructuring costs

-

498

Adjusted EBITDA

3,320

$

1,514

$ |

Thirteen Weeks

Ended March 29, 2014

March 30, 2013

Net sales

68,028

$

65,405

$

Cost of sales

(1)

47,327

45,667

Gross profit

20,701

19,738

Operating expenses:

Marketing

10,115

11,191

General and administrative

4,147

4,687

Fulfillment

4,712

5,381

Technology

1,148

1,515

Amortization of intangible assets

84

106

Total operating expenses

20,206

22,880

Income (loss) from operations

495

(3,142)

Other income (expense):

Other income (expense), net

(3)

7

Interest expense

(259)

(187)

Total other expense, net

(262)

(180)

Income (loss) before income tax provision

233

(3,322)

Income tax provison

32

21

Net income (loss)

201

(3,343)

Other comprehensive income (loss), net of tax:

Foreign currency translation adjustments

8

(6)

Total other comprehensive income (loss)

8

(6)

Comprehensive income (loss)

209

$

(3,349)

$

Net income (loss) per share:

Basic

$

0.00 (0.11)

$

Diluted

$

0.00 (0.11)

$

Weighted average common shares outstanding:

Basic

33,384

31,141

Diluted

34,158

31,141

21

Consolidated Statements of Comprehensive Operations

(Unaudited, in Thousands, Except Per Share Data)

(1)

Excludes

depreciation

and

amortization

expense

which

is

included

in

marketing,

general

and

administrative

and

fulfillment

expense. |

March 29

December 28

ASSETS

2014

2013

Current assets:

Cash and cash equivalents

1,392

$

818

$

Short-term investments

39

47

Accounts receivable, net of allowances of $152 and $213 at

March 29, 2014 and December 28, 2013,

respectively 4,882

5,029

Inventory

36,613

36,986

Other current assets

2,959

3,234

Total current assets

45,885

46,114

Property and equipment, net

18,810

19,663

Intangible assets, net

1,517

1,601

Other non-current assets

1,720

1,804

Total assets

67,932

$

69,182

$

LIABILITIES AND STOCKHOLDERS' EQUITY

Current liabilities:

Accounts payable

21,469

$

19,669

$

Accrued expenses

6,867

5,959

Revolving loan payable

750

6,774

Current portion of capital leases payable

277

269

Other current liabilities

5,383

3,682

Total current liabilities

34,746

36,353

Capital leases payable, net of current portion

9,431

9,502

Deferred income taxes

65

335

Other non-current liabilities

2,125

2,126

Total liabilities

46,367

$

48,316

$

Stockholders' equity:

Series A convertible preferred stock, $0.001 par value; $1.45

per share liquidation value or aggregate of $6,017;

4,150 shares authorized; 4,150 shares issued and

outstanding at March 29, 2014 and December 28, 2013,

respectively 4

4

Common stock, $0.001 par value; 100,000 shares authorized;

33,413 and 33,352 shares shares issued and outstanding

at March 29, 2014 and December 28, 2013, respectively

33

33

Additional paid-in capital

169,243

168,693

Common stock dividend distributable

59

60

Accumulated other comprehensive income

454

446

Accumulated deficit

(148,228)

(148,370)

Total stockholders' equity

21,565

20,866

Total liabilities and equity

67,932

$

69,182

$

22

Consolidated Balance Sheet

(Unaudited, in Thousands, Except Par and Per Share Liquidation value)

|